That’s not an uncommon view. And viewed purely in monetary terms, financial advice IS expensive.

But what if we told you that it can be less expensive than not getting financial advice?

Research over the past few years has shown that good financial advice can save you much more than it costs you.

A 2019 report by Vanguard estimated that clients who are advised (rather than those who invest money via online platforms or under their own steam) can add around 3% to their overall returns.

The International Longevity Study reckoned that your pension pot can be 50% bigger as a result of working with a financial planner on a long-term basis.

How can talking to an adviser make that much difference?

Spoiler alert: it’s not because we have the inside track to the hot performing stocks and shares. We have no more idea than you do when Elon Musk is about to declare his fondness for a new cryptocurrency, and we can’t spot the next GameStop. (Don’t believe others if they say they can.)

There are four key reasons why professional financial planning is worth paying for.

1. We turn dreams into goals

A financial planner starts by finding out what you’re looking to achieve with your money. What are your long-term goals? Where are you now, and where do you want to be in the future?

Rather than just building an investment portfolio that hopes to gain X% per year, we help you articulate what you want your money to do for you – let you retire at 55, travel extensively, build your ideal home from scratch… whatever.

Then, we look at your income and outgoings, assets and liabilities, and work out a plan that turns your dreams into achievable goals. If you want to take a round-the-world trip in ten years’ time, buy a home for your children to live in when they’re at university, upgrade your family car every three years, sell your business in five years, we factor that into the plan and create a route map that builds in those destinations along the way.

This doesn’t mean waiting for the good times to arrive. Life is for living, so your plan will allow you to do want you want now, without worrying that you’re jeopardising your future goals.

Why is this worth it?

When you have a target to hit, you’re less likely to lose focus. You know what you’re working towards and, more to the point, you know you can achieve it and how you can achieve it. You’re not just investing and hoping for the best.

2. We manage your tax

Managing your finances isn’t just about what you invest and spend. All of us above a certain level of income have to pay tax. It’s part of our job to ensure your tax obligations are fulfilled while minimising your outgoing costs.

By carefully structuring your finances, we ensure you make the most of your allowances for income and capital gains tax, dividends, ISAs, pensions and other tax wrappers.

3. We take appropriate levels of risk

Given that there’s a wealth of evidence about what works and what doesn’t when it comes to investing in the stock market, it’s frankly incredible that many financial professionals still advocate treating portfolio management like a trip to the casino.

A good financial planner will choose carefully where to put your money and base their decision on peer-reviewed research. We call it evidence-based investing because that’s what it is: investing based on evidence, not a hunch or some special human stock-picking skill that hits the heights one year and fizzles out the next.

Your portfolio is structured to deliver the goals you want to achieve. It balances risk: spreading investment in different asset classes and global markets. So although we’d expect the asset classes in your portfolio to deliver positive returns in the long run, they will inevitably perform quite differently over short periods.

4. We save you from yourself

However much you think everything is in control, there will always be something that comes along that looks set to derail all your plans. Stock market crashes, freak weather, wars and pandemics – those four horsemen of the apocalypse have each hit the world more than once in the last couple of decades.

It’s understandable, when you hear news reports of the ‘biggest stock market fall for a century’, to want to sell up to avoid losses.

But look at history.

In the vast majority of cases, stock market crashes are followed fairly rapidly (in investing terms) by stock market recoveries.

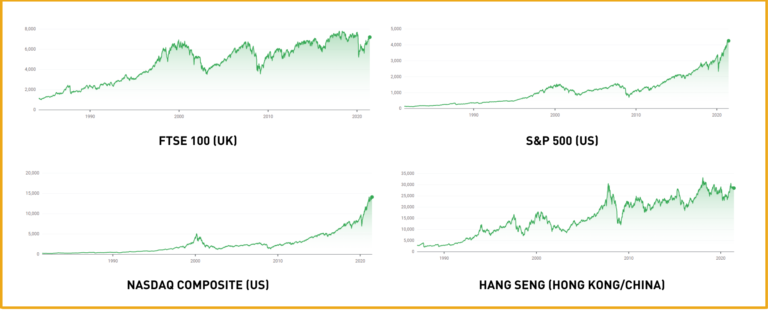

Here are four key stock market indices over a 30-40 year period. Bear in mind this timescale includes Black Monday (1987), the Dotcom Bubble of the early 2000s, the Global Financial Crisis of 2008-9 and Coronavirus (2020).

You can see that the key markets are on a long term upward trajectory and recovered fairly quickly from all four of the most recent crashes.

Now imagine if you’d panicked in February 2020 when markets everywhere went into freefall. If you’d sold in response to that, you would have missed the gains you can clearly see since then – especially in the US, where most of the big tech stocks that have soared in the pandemic (think Amazon, Microsoft, Zoom etc.) are based.

It’s hard to hold on when everyone else is selling or be circumspect when everyone else is buying. It’s the job of a financial planner to ‘hold your hand’ through these wobbles, however dramatic they may seem at the time, and help you avoid making expensive mistakes.

With a globally diversified portfolio held over the long term, most of our clients will have seen the benefits of these gains.

When we ask our clients the main reason they use a financial planner, they tell us it’s peace of mind, clarity for the future and the confidence to retire earlier than they ever thought possible.

And if that isn’t worth talking to a professional, we don’t know what is.

As F. Scott Fitzgerald, creator of The Great Gatsby said, “The very rich are different from you and me.” They do have unimaginable wealth, but they also have the opportunity most of us don’t – to change the lives not only of themselves, but of millions of others around the world.

Bill and Melinda Gates have pledged to give 95% of their wealth away and have established the world’s biggest private charitable foundation, with an estimated $51 billion in assets. Together with Warren Buffett, widely described as the world’s greatest investor, they created The Giving Pledge, signing up many of the world’s richest philanthropists who have vowed to give away the majority of their wealth either before or after their death.

Buffett has committed to giving away 99% of his Berkshire Hathaway stock – the source of his great fortune. Explaining his decision, he said, “My luck was accentuated by my living in a market system that sometimes produces distorted results, though overall it serves our country well.

“I’ve worked in an economy that rewards someone who saves the lives of others on a battlefield with a medal, rewards a great teacher with thank-you notes from parents, but rewards those who can detect the mispricing of securities with sums reaching into the billions. In short, fate’s distribution of long straws is wildly capricious.

“The reaction of my family and me to our extraordinary good fortune is not guilt, but rather gratitude. Were we to use more than 1% of my claim checks [Berkshire Hathaway shares] on ourselves, neither our happiness nor our well-being would be enhanced.

“In contrast, that remaining 99% can have a huge effect on the health and welfare of others. That reality sets an obvious course for me and my family: keep all we can conceivably need and distribute the rest to society.”

What is real wealth?

Few of us can hope to match the wealth of Buffett or the Gateses. But financial wealth, above and beyond that which we need to look after ourselves and our families now and in the future, gives us perhaps two of the greatest luxuries of all: choice and time.

Choice, because we can afford not to have to do things we’d rather not, simply because we need the money.

And time, because we are in control of how we spend our hours and days – whether that’s working or playing.

These luxuries don’t depend on us being rich – certainly not in Gates or Buffett terms, and not even in terms that most of us would use to define what we mean by ‘rich’.

We don’t need 10-bedroom mansions to feel rich. We don’t need a yacht, several fast cars or five long-haul holidays a year (although we may be craving some time on the beach after the year we’ve all just had).

What does real wealth mean to you? Is it, like Bill and Melinda Gates and Warren Buffett, the ability to change the lives of millions of people you will never know personally.

Or is it, as one of our clients recently told us, as simple as, “being able to nap whenever I want”

It’s everyone’s dream… retiring when we’re still young enough to enjoy life, with enough put by in our pension pot, savings and investments to finance the life we want to live until the day we meet our maker.

But with the average UK pension pot standing at just over £61,000 after a lifetime of saving, you’re going to have to plan to achieve that dream lifestyle, and balance your spending to avoid depleting your savings.

Here’s how planning ahead and using your money wisely can help you fund the retirement you really want.

First things first: talk to a financial planner

We would say that, wouldn’t we? But it’s true. Research by The International Longevity Centre UK revealed that just by taking professional advice, UK savers improve their pension savings alone by £30,991.

Don’t take everything from the same pot

By the time you retire, you may have a collection of different savings and investment pots: a pension, an ISA, bonds, a trust fund, for example. But don’t make the mistake of treating them the same and withdrawing from them without a tax-efficient strategy.

Every savings and investment vehicle you have is effectively a ‘tax wrapper’ for a chunk of money you are putting by for the future. And different tax wrappers are taxed in different ways and at different rates.

Generally speaking, you should withdraw from your least-expensive asset first – the ones that are earning you least interest, or those that are non-taxable so withdrawing from them doesn’t incur any tax liability. But don’t drain one asset before you start on the next. Remember, you should still be looking to have a portfolio that’s balanced in line with the risks you’re prepared to take.

And speaking of risks…

Don’t be too cautious

As a retiree, your focus should be on preserving your financial security. You’re living on the wealth you accumulated in your years of productive earning. But you still need that wealth to work for you. So don’t pull everything out of the stock market and put it all into ‘safe’ assets like bonds. Your portfolio will have been planned to last you until the end of your days, and to do that, it will still need to be invested to keep up with inflation, which erodes your spending power.

Avoid taking your state pension too early

In the UK, the state pension age is 66 for men born after 1951 and women after 1953. But the longer you delay taking your pension beyond age 66, the more it will be worth when you do take it. You’ll get an extra £10.42 per week if you delay taking it for one year, for example – that’s over £500 per year.

You can take 25% of your private pension tax-free from age 55, which can be handy if you have enough in the remaining 75%, plus your state pension and any other investments, to fund your retirement. But be careful: depending on how your private pension is invested, you may not be able to draw down that tax-free sum without triggering the rest of your pension paying out at the same time – either as a taxable lump sum or an annuity you don’t want or need until you retire.

It’s not about the returns

Throughout your investing life, you’ve probably paid a lot of attention to the returns your investments are making, But as a retiree, it’s all about what your investments can buy you.

An annuity, for example – the default option for most pension schemes – can give you a predictable fixed income based on gradually reducing the money in your pot. But you may want to balance this with withdrawing from your other investments at a consistent percentage every year, or taking the dividends you may otherwise have reinvested in your earning years.

Don’t spend it all at once

When your income is unlinked from your earnings and your assets are in front of you, waiting to be spent, it’s perhaps understandable to loosen the reins on your budget and splash out on things you wouldn’t otherwise have done if you were still living off a monthly salary.

It’s tempting, too, to see the money you’re no longer spending on commuting, buying smart clothes for the office and expensive lunches as money available to spend on ad-hoc, unplanned treats. (A lot of people found this out the hard way when working from home in lockdown, only to see spending increase dramatically again as they started going back to the office and booking holidays.)

But don’t forget that, even though your retirement lifestyle may cost less on a day-to-day basis, you probably still want to spend on planned activities such as holidays, financing grandchildren’s education or doing up the house. And as we get older, health and care costs will increase.

It’s a good idea to talk to a professional about building these additional costs into your spending plans as the years go by. And right from the start, set a budget for your regular expenses and any discretionary spending you have. You won’t be able to rely on annual pay rises to offset inflation, so make sure that’s worked into your budget, too.

Agree with your partner

It’s vital if you’re planning for retirement as a couple that you and your partner agree on how you handle your finances, especially if you were reasonably financially independent of each other in your pre-retirement life. One of you may be a lot more risk-tolerant than the other, which was fine when you were both earning your own income, but you need to make sure that you are both comfortable with your retirement finances.

A financial adviser or coach can steer a middle way through differing expectations.

Is that £1 million-worth of advice?

If all of this sounds like sensible but pretty standard advice, and nothing that would make a million pounds-worth of difference to your finances, think again.

We recently took on clients who had built significant wealth throughout their working lives and had recently sold their business, which added to the amounts they already had.

After a discussion around what they wanted the balance of their lives to be about, we were able to put a framework in place to help them live the very comfortable lifestyles they were used to, to never worry about money again and to reduce their personal tax liabilities significantly. We were able to calculate that our planning together would save and make them over £3m!

Perhaps the biggest difference you can make to your retirement income is to get professional advice. You don’t need to be mega-wealthy to see a significant impact on your finances… and on your peace of mind.

The small print: past performance is no guarantee of future results

“The yield curve is flattening (or growing steeper)! … Yield curve spreads are widening (or narrowing)! … The yield curve has inverted (or normalised)!”

Headline-grabbing yield curve commentary somehow sounds important, doesn’t it? But what is a yield curve to begin with, and what does it have to do with you and your investments?

A Tour Around the Curve

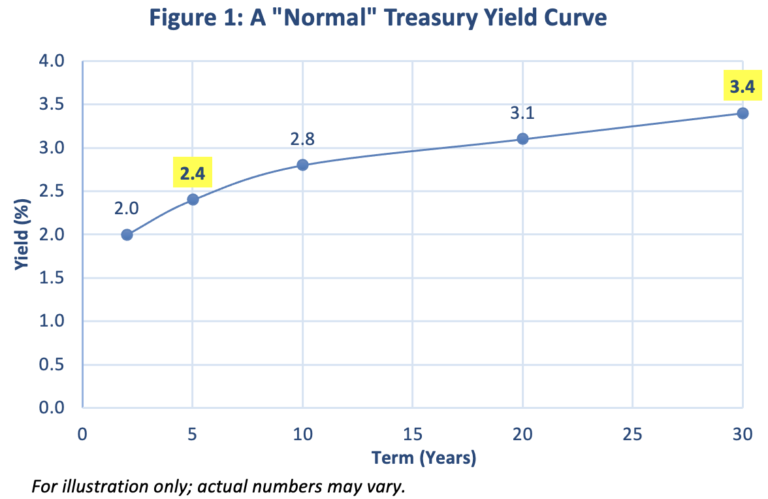

Yield curves typically depict the various yields across the range of maturities for a particular bond class. For example, Figure 1 would inform us that a Treasury bond with a 5-year maturity was yielding 2.4% annually, while a 30-year Treasury bond was yielding 3.4%.

Bond class – A bond class or type is typically defined by its credit quality. Backed by the full faith of the government, U.S.Treasury yield curves are among the most frequently referenced, and often the high-quality benchmark against which other bond types are compared – such as municipal bonds, corporate bonds, or other government instruments.

Term/Maturity – The data points along the bottom X axis of a yield curve represent various terms available for a bond class. The term is the length of time you’d need to hold a bond before your loan matures and you should receive your initial investment back.

Yield – The data points along the vertical Y axis represent the interest rate, or yield to maturity currently being offered – such as 2% per year, 3% per year, and so on. The yield curve for any given bond class changes every time its yields change … which can be frequently.

Spread – The spread is the difference between the annual yields on two bond maturities. So, in Figure 1, there’s a 1% spread between 5-year (2.4%) and 30-year (3.4%) Treasury bond yields.

Define “Normal”

Next, let’s look at the curve itself – i.e., the line that connects the data points just discussed.

The shape of the yield curve helps us see the relationship between various term/yield combinations available for any given bond class at any given point in time.

Just as our body temperature is optimal around 98.6°F (37°C), there’s a preferred equilibrium between bond market terms and yields. “Normal” occurs when short-term bonds are yielding less than their longer-term counterparts. Under normal economic conditions, investors expect to be compensated with a term premium for taking the incremental risk of owning longer maturities. They’re accepting more uncertainty about how current prices will compare to future possibilities. Conversely, they’ll accept lower rates for shorter-term instruments, offering greater certainty.

At the same time, evidence suggests there’s often a law of diminishing returns at play. Typically, the further out you go on the yield curve, the less extra yield is available. Thus, Figure 1 depicts a relatively normal yield curve, with a bigger jump to higher returns early in the curve (a steeper spread) and a more gradual ascent (narrower spread) as you move outward in time.

Variations on the Curve

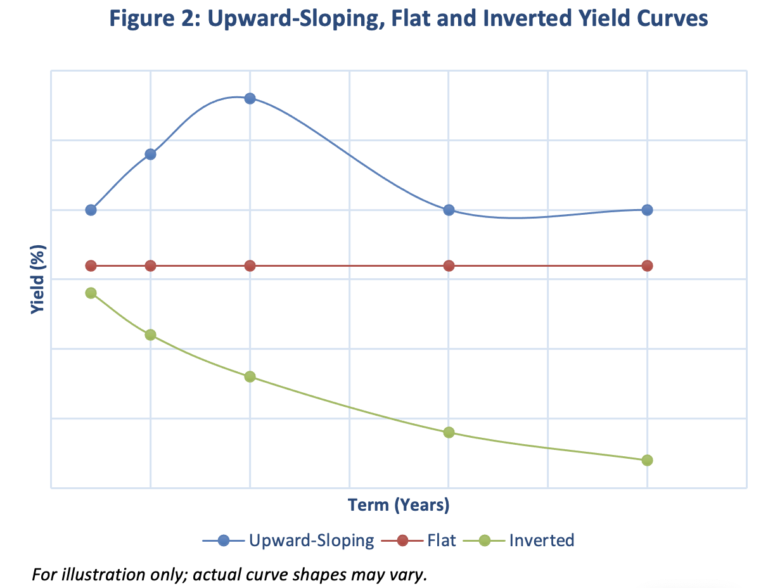

If Figure 1 depicts a normal yield curve, what happens when things aren’t so normal, which is so often the case in our fast-moving markets?

The shape of the yield curve essentially reflects evolving investor sentiments about unfolding economic conditions.

In short, expectations theory suggests that the yield curve reflects investor expectations of future interest rates at any given point in time. Thus, if investors in aggregate expect rates to rise (fall), the yield curve will slope upward (downward). If they expect rates to remain unchanged, it will be flat. Figure 2 depicts three different curve shapes that can result.

You, the Yield Curve and Your Investments

It’s rare for the yield curve to invert, with long-term yields dropping lower than short-term. But it happens. This typically is the result of a country’s central bank tightening monetary policy, i.e., driving up short-term rates to fight inflation. An inverted yield curve is often followed by a recession – although not always, and not always universally.

Does this mean you should head for the hills if the yield curve inverts or takes on other “abnormal” shapes? Probably not. At least not in reaction to this single economic indicator.

As with any other data source, bond yield curves are best employed to inform and sustain your durable, evidence-based investment plans, rather than to tempt you into abandoning those plans every time bond rates make a move. Big picture, this typically means investing in bonds that offer the highest yield for the least amount of term, credit and call risk. (Call risk is realised if the bond issuer “calls” or pays off their bond before it matures, which usually forces the bond’s investors to accept lower rates if they want to remain invested in the bond market.)

The yield curve is an important tool for determining how to efficiently execute this greater goal. It helps explain why we typically recommend holding only high-quality bonds, minimising call risk, and usually striking a balanced middle ground between short-term versus long-term bonds. Similar principles apply, whether investing directly in individual bonds or via bond funds.

In short, it’s fine to consider the yield curve, but it’s best to look past it to the distant horizon as you invest toward your steadfast financial goals. We hope you’ll be in touch if we can tell you more about how fixed income/bond investing best fits into that greater context.

What does half of the UK adult population have in common with Abraham Lincoln, Kurt Cobain and Amy Winehouse?

The answer is probably more prosaic than you’d imagine: they died without leaving a will.

But the 54% of adults and 60% of parents in this country who, reportedly, have not created a will are removing themselves from important decisions about what happens to their own money and assets when they die.

What happens if you die without a will?

Dying intestate (the legal term for ‘without a will’) can raise problems, whatever your marital or relationship status.

Your estate will be divided up according to the rules of intestacy, which don’t take your feelings or family dynamics into account. Your worldly goods could be passed on either to people you’d rather didn’t have them, to people you hardly know or, failing that, to the state.

The rules are slightly different depending which part of the UK you live in, but consider the following if you die without leaving a will:

Your partner is not legally entitled to anything unless you’re married or in a civil partnership, however long you have been together

This means your children, grandchildren or other beneficiaries can, if they wish, legally cut your partner out of your estate — not only the money you leave but the home they live in, if it’s held in your name only

On the other hand, if you are married or in a civil partnership, your spouse or partner could inherit everything even if you’re separated (except in Scotland), leaving your children with nothing

If you die with no close relatives, everything could go to the government, who benefited to the tune of £8 million last year from people who died intestate.

However stable and ‘normal’ your personal life may be to you, families and relationships are more complicated than ever these days. It’s not unusual for the offspring of separated or divorced parents to have half-siblings in two different families as well as their own — more if there’s more than one separation down the line. And if relationships turn sour, it could be there are children and grandchildren you don’t even know about, all of whom could be entitled to a share of the estate.

But a will is about more than money. If, God forbid, you and your partner both die while your children are still young, a will allows you to nominate who will look after them and how the money from your estate may be used to support them before they are old enough to inherit in their own right

Where there’s a will, there is also tax planning

Your estate could be liable to more inheritance tax (IHT) if you have not been specific about distributing your assets, leaving whoever ends up inheriting your estate with an IHT headache which could see 40% of your assets being claimed by the government and clawed back from the beneficiary — probably not something you would have wanted.

An IHT liability can be mitigated by efficient tax planning, which focuses, perfectly legally, on keeping your taxable liabilities below the inheritance tax threshold (currently £325,000 for individuals).

Inheritance tax can be reduced by:

giving away your assets — as well as gifting sums on an annual basis that are free from tax, you can give away any assets (like your home*) and, providing you survive for at least seven years afterwards, the recipients of those assets will not be liable for inheritance tax

placing assets in a trust — this will remove them from your estate, and so from an IHT liability (subject to the 7-year rule)

insuring against IHT and place the policy in a trust

passing on assets that have depreciated — these will not be liable to capital gains tax and, if they do start appreciating again, the gain (and potential IHT liability) will be for the recipient and not your estate

leaving a charitable legacy — many people leave money to charity in their will (encouraged not only by philanthropy but by initiatives such as Free Wills Month), and any charitable legacy you leave will be free of IHT. If you leave more than 10% of your residual estate to charity, the IHT liability on your remaining estate will reduce, too.

Don’t forget your pension

If you die before you are 75, your pension policy can pay out a tax-free income or lump sum to anyone who is classed as a dependent (including your spouse or partner and children).

But if you don’t have any financial dependents, other beneficiaries could receive a lump sum which would then form part of their estate and potentially be liable to inheritance tax when they die.

To avoid passing on this tax liability, you must nominate individuals you’d like to benefit from a tax-free income instead.

Taking care of business

Your untimely death, with or without a will, would be devastating for your family. But if you’re also a shareholding director of a business, it may create issues for your fellow shareholders, too.

If you die while still in post, your shares form part of your estate and go to your beneficiaries. And while you’ll want your family to benefit from the value of those shares, it’s likely neither you or your fellow shareholders will want unqualified or uninterested relatives having a controlling share in the business after your death.

You can avoid this by creating a business continuity plan, with life insurance arranged on the life of each of the shareholders to benefit the surviving shareholders. This will mean your fellow directors can rely on having enough funds to buy the shares back from your beneficiaries, while allowing your nearest and dearest to receive the financial value of your shares.

March is Free Wills Month, where participating solicitors will create or update a simple will for free. It’s backed by charities who hope you will take the opportunity to remember their good cause in your estate planning.

If you’d like to discuss tax and estate planning, please get in touch with Kevin Wood at Oak Four to arrange a no-obligation consultation.

*There are additional rules around gifting your home to others, and you should seek legal advice before taking any action to reduce your potential IHT liability.

If there’s one thing the past year has taught us, it’s that there are things in life we can’t control.

There are even things that governments (well, most of them) can’t control. And if the people in charge can’t call the shots, what hope is there for the rest of us?

Control freakery is rarely a successful state of mind. So should we just give up and go with the flow?

We’d say not. From a financial point of view, as in life generally, wellbeing comes from recognising what you can and can’t control.

As Clare Seal, author of ‘Real Life Money’ put it, financial wellbeing is, “the feeling of having achieved a degree of separation between your net worth and your self-worth. It’s a state of relative steadiness, an equilibrium whereby you feel confident and equipped to deal with the money curveballs that life throws your way.”

And the government’s Financial Capability Strategy for the UK reported that that over 60% percent of people didn’t feel they could determine what happens in their lives when it comes to money, with 47% not feeling confident about making decisions about financial products and services.

It’s not only whether you think you have enough for now that affects your wellbeing, but whether you feel confident about the future and able to withstand any bumps in the road.

It’s hard to imagine anything as massive as Covid happening again, but experts say it’s unlikely to be the last pandemic in our lifetime. Add to this the impact of climate change on the way we live our lives — even if we do manage to avoid the worst by comprehensive international co-operation — and it’s tempting to throw your hands up in the air whilst simultaneously burying your head in the sand.

You can’t control global geo-political events. You can’t control the stock market, either, despite what some advisers claim.

But you can, to a great extent, take control of your own financial future, and that of your family, and in doing so achieve the financial wellbeing that will impact positively on your mental health.

Where do you start?

One word: goals.

It’s not just about how much you earn or what you’re worth but knowing where you want to be and what it takes to get you there.

And, most importantly, it’s having the confidence that you can afford to do what you want to do without worrying.

Your goals could be anything, for example:

I want to retire at 55

I want to take a couple of years off to travel in my late 40s

I want to give my kids a financial boost when they leave home

I’d like my grandchildren to be educated privately

I want to sell my business in five years

I’d really love a sports car

I want to support causes that mean a lot to me

I’d love to be able to take four holidays a year

You might look at that list and feel very few of those goals are achievable to you. But you’d be surprised. It’s perfectly possible to achieve your future goals if you have the right financial tools in place and make the most appropriate investment choices.

When you talk to us at Oak Four, you’ll realise very soon that our emphasis isn’t just on making money, and we certainly don’t chase the latest craze. (GameStop, anyone?)

Instead, we look at how you want to live and what you want your future to be, and work back from there.

It’s not about sacrificing luxuries and experiences in the short term but recognising what’s important to you in the long term and putting the plans in place to make it happen.

As with most things in life, the sooner you start, the better. You don’t have to have a huge amount of money to invest, just the knowledge of what you want to achieve.

If you’d like to talk to us about putting your financial plan into place, book a free call to get the ball rolling.

“You can’t invest without trading, but you can trade without investing. … thinking you’re investing when all you’re doing is trading is like trying to run a marathon by doing 26 one-mile sprints right after the other.” — Jason Zweig

Are you out of breath trying to keep up with the breaking news about GameStop (GME) and all the other red-hot trades of the day? Here’s a synopsis (to date), and what it means to you as an investor.

Seemingly Unstoppable Games: Last week, a perfect storm of traders converged on the market, propelling the prices of a few previously sleepy stocks into the stratosphere. Jason Zweig of The Wall Street Journal reported, “From Jan. 25 through Jan. 29, a ragtag army of individuals sent shares in GameStop Corp. up 500%, and sent many others skyrocketing too.”

Reddit Gone Wild: Interestingly, there was no huge, breaking news or major shift in these companies’ fundamentals to explain the surge. Instead, a tidal wave of trading momentum happened to form on a Reddit forum called WallStreetBets.

Keith Gill (aka, Roaring Kitty, aka DeepF***ingValue): If the GameStop movement had a leader – or at least a cheerleader – it might have been Gill, who had been entertaining his online friends with GameStock status reports since he began trading it in spring 1999. The Wall Street Journal reported, “Mr. Gill said he wasn’t a rabble-rouser.” But, the report continued, “Many online investors say his advocacy helped turn them into a force powerful enough to cause big losses for established hedge funds.”

Big Short-Sellers Get Squeezed: Whatever inspired the movement, it soon became a force of its own, like an online flash mob buying and holding shares at increasingly higher prices. Why would anyone do this? Some may have just gotten caught up in the excitement. Even Elon Musk got in on the action with his “Gamestonk!!” WallStreetBets tweet. Others were hoping to profit on a communal squeeze play against “fat cat” hedge funds and others who had chosen to short-sell the same stocks.

When a trader short-sells a stock, they’re betting the price is about to drop. If it does, they can profit handsomely. But if the price instead shoots upward, a short-seller can face a margin call, requiring them to cough up the difference between the original share value and the fast-soaring price. In the case of GameStop, short-sellers like Melvin Capital Management lost billions of dollars meeting margin calls, which in turn became chum to the feeding frenzy.

Robinhood Parries: As the frenzy continued, many retail trading platforms – including Robinhood, Schwab, TD Ameritrade, and others – started experiencing trading overloads. Technical glitches as well as deliberate trading restrictions ensued. Not surprisingly, traders impacted by the lapses and restrictions have cried foul, perhaps rightfully so.

Enter the Fed: Is the phenomenon just a new, but legal variation on a very old market mania theme? Did anyone actually violate existing regulations, and if so, whom? Are new regulations warranted? Securities regulators are considering these questions, not yet resolved.

Now, to the main point. Where does this leave YOU as an investor?

You may have noticed: As we’ve introduced the players in this unfolding drama, we’ve not used the term “investor.” That’s because none of them are, in fact, investing. Not the retail traders flexing their communal muscle. Not the short-sellers who lost their shirts. Not the trading platforms, stuck in the middle.

Everything we’ve been describing so far has involved trading, where there’s nothing new about having big winners and sore losers. By definition, trading is a messy, cut-throat, zero-sum game. For every trader who gets to buy low and sell high, there must be a pair of traders on the other side, who were willing to sell low and buy high. The only real questions in the current drama are whether any rules were broken that made the trades illegal, or whether any new rules need to be crafted to ensure markets don’t become so unstable, they cease to operate.

As proponents of relatively efficient markets, we remain confident these questions will be resolved. It may not be pretty, but this too shall pass.

In the meantime, be an investor, and remain one.

Over time and around the globe, winning and losing traders converge, and create market growth. Their volatile trading games translate into long-term market returns. As an investor, you can capture these returns by buying and patiently holding broad market positions, based on your willingness, ability and need to take on investment risks in exchange for expected market returns.

As an investor, it really is that simple, and we’re here to help you do just that. As a trader? Wow, if anything, these recent adventures in trading land should underscore (with a thick, black Sharpie®!) how impossible it is to predict where any given stock, sector, or forecast is headed next. All the more reason to bet on the efficiency of a long-term, globally diversified portfolio, and to leave the GameStop gambles to the traders. Let us know if we can assist further with that.

Remember when you were a teenager? It’s probably the richest you’ve ever been in your life.

You were still living rent-free with your parents, with few or no expenses to speak of. Virtually everything you earned from your pocket money or part-time job was yours to do with as you wished.

How many of us would love to return to the sort of financial freedom we had in those days?

Financial freedom is the driving force behind the FIRE (Financial Independence Retire Early) movement.

FIRE aficionados prioritise saving and investing as much as possible, along with spending less, in their most profitable working years. This means they can stop working much sooner than most people and live off the income generated by their investments and previous frugal lifestyle.

Don’t know about you, but spending more than a few hours a month tending to your investments doesn’t sound like a peaceful ‘retirement’ to us.

And as evidence-based advisors, we wouldn’t advocate continual churning of your portfolio to try and maximise returns, even – especially – in turbulent times like these.

Many FIRE advocates are prolific active investors, whose focus is spotting stocks that are ‘hot’ and trading them to maximise returns. It’s a risky strategy and one no evidence-based investor would choose to follow.

But retiring early? Super-early? That doesn’t sound like such a bad idea.

So how do you do it without risking everything and staying true to your evidence-based principles?

Planning is the key

Like most successful lifestyles, the key is to start early and plan thoroughly.

But don’t forget: the frugal lifestyle you allocate yourself in your early 20s, saving half of what you earn and living on baked beans, may be trickier to maintain as you progress through different life stages.

Starting a family, especially, can be like turning on a money tap that takes 20 years to turn off.

Sitting down with an evidence-based financial planner as soon as possible will give you a head start on making your FIRE dreams come true.

Enthusiasm and excitement can only take you so far. Setting goals and then creating a financial roadmap will give you more of a chance of achieving them.

Let’s say you’re 25 and you want to achieve financial freedom when you’re 45. That’s more than 20 years (at least) before most people retire.

You can look forward to the state pension (as long as you’ve contributed at least 10 years’ worth of national insurance payments), and any occupational or private pension. But you won’t be able to access these, as things stand, until you’re at least 66 (for the state pension) and 55 (for private provision) respectively.

Don’t forget you’ll need 35 qualifying years of NI payments to get the new full State Pension if you do not have a National Insurance record before 6 April 2016.

How will you fund those 20 pre-pension years (and beyond, if you want to live comfortably)?

You can assume you’ll continue to earn a reasonable amount before you’re 45. But don’t presume your expenses will stay the same, even if you forego things like a car, foreign holidays or private education for your kids.

An evidence-based financial planner will be able to build a roadmap to age 45 which takes into account most of the predictable turns and diversions life will throw at you.

What does ‘retirement’ mean?

The traditional view of ‘retirement’ is ‘stopping work and enjoying life’.

Of course, this implies that you don’t enjoy work, which isn’t always the case. But implicit within the term ‘retirement’ is doing very little, apart from hedonistic pursuits such as long holidays and plenty of gardening.

If you retire in your 40s it’s unlikely that you’ll be ready to settle down with a trowel and a seed catalogue.

Many FIRE advocates have made this mistake, though, notably blogger Finimus:

“I’m fairly sure that when I was saving hard in my 20’s I had the vague idea that my future multi-millionaire self would be spending his days lounging around on his private sun-bleached Caribbean island draped in nubile dusky maidens, or perhaps heli-skiing with super-models in the Alps. What wasn’t in mind: doing the grocery shop, popping some washing on, un-packing the dish-washer, and then picking my daughter up from hockey club. Sure – these are all things that need doing, but they aren’t very exciting, are they? This is more house-husband than super-rich.”

Stop work in your 40s, and even with the finances well taken care of, you’ll still probably have relatively young children to support, along with, perhaps, elderly parents to care for.

More to the point, life is boring without a sense of purpose. For most of us, that sense of purpose is covered by ‘work’, which exists primarily to help us fund ‘life’.

Those who have made sense of FIRE, like Mr Money Mustache, still do some form of work to keep things ticking over; but a lot less, and a lot more enjoyably, than they would have done in their pre-FIRE days.

Even if you are lucky enough to be able to live completely and fully on your investments, there are only so many cruises you can go on.

Stopping work at 45 means you probably have another 45 years to fill.

Plan how you’re going to spend those years, as well as how you’re going to fund them, and you could make FIRE work for you.

It’s certainly understandable if the economic uncertainty unfolding in the daily news has left you wondering – or worrying – about what’s coming next. No matter how you feel about the U.S. entering into a trade war with China, or a potential no-deal Brexit, it’s hard to deny that the prospect is currently causing considerable market turmoil.

Regardless of how the coming weeks and months unfold, are you okay with gritting your teeth, and keeping your carefully structured portfolio on track as planned? This probably doesn’t surprise you, but that’s exactly what we would suggest. (Unless, of course, new or different personal circumstances warrant revisiting your investments for reasons that have nothing to do with all the tea in China.)

That said, the news is admittedly unsettling. If you’ve got your doubts, you may be wondering whether you should somehow shift your portfolio to higher ground, until the coast seems clear. In other words, might these stressful times justify a measure of market-timing?

Here are four important reminders on the perils of trying to time the market – at any time. It may offer brief relief, but market-timing ultimately runs counter to your best strategies for building durable, long-term wealth.

Market-Timing Is Undependable. Granted, it’s almost certainly only a matter of time before we experience another recession. As such, it may periodically feel “obvious” that the next one is nearly here. But is it? It’s possible, but market history has shown us time and again that seemingly sure bets often end up being losing ones instead. Even as recently as year-end 2018, when markets dropped precipitously almost overnight, many investors wondered whether to expect nothing but trouble in 2019. As we now know, that particular downturn ended up being a brief stumble rather than a lasting fall. Had you gotten out then, you might still be sitting on the sidelines, wondering when to get back in. The same could be said for any market-timing trades you might be tempted to take today.

Market-Timing Odds Are Against You. Market-timing is not only a stressful strategy, it’s more likely to hurt than help your long-term returns. That’s in part because “average” returns aren’t the near-term norm; volatility is. Over time and overall, markets have eventually gone up in alignment with the real wealth they generate. But they’ve almost always done so in frequent fits and starts, with some of the best returns immediately following some of the worst. If you try to avoid the downturns, you’re essentially betting against the strong likelihood that the markets will eventually continue to climb upward as they always have before. You’re betting against everything we know about expected market returns.

Market-Timing Is Expensive. Whether or not a market-timing gambit plays out in your favor, trading costs real money. To add insult to injury, if you make sudden changes that aren’t part of your larger investment plan, the extra costs generate no extra expectation that the trades will be in your best interest. If you decide to get out of positions that have enjoyed extensive growth, the tax consequences in taxable accounts could also be financially ruinous.

Market-Timing Is Guided by Instinct Over Evidence. As we’ve covered before, your brain excels at responding instantly – instinctively – to real or perceived threats. When market risks arise, these same basic survival instincts flood your brain with chemicals that induce you to take immediate fight-or-flight action. If the markets were an actual forest fire, you would be wise to heed these instincts. But for investors, the real threats occur when your behavioral biases cause your emotions to run ahead of your rational resolve.

We’d like to think one of the most important reasons you hired a financial adviser is to help you avoid just these sorts of market-timing perils – during just these sorts of tempting times. Even if you do everything “right” in theory, we still cannot guarantee your success. But we are confident that sticking with your existing plans represents your best odds in an uncertain world.

So, if you have your doubts, please let us know. It’s our job – not to mention our moral and fiduciary imperative – to offer you our best advice across all of the market’s moves. While market-timing may be illusory, we are here for you, ready to explore various real steps you can take to shore up your investment resolve, regardless of what lies ahead.

Thanks to Dimensional Fund Advisors for this guest post.

Focusing on what you can control can lead to a better investment experience.

Whether you’ve been investing for decades or are just getting started, at some point on your investment journey you’ll likely ask yourself some of the questions below. Trying to answer these questions may be intimidating, but know that you’re not alone. Your financial adviser is here to help. While this is not intended to be an exhaustive list it will hopefully shed light on a few key principles, using data and reasoning, that may help improve investors’ odds of investment success in the long run.

What sort of competition do I face as an investor?

The market is an effective information-processing machine. Millions of market participants buy and sell securities every day and the real-time information they bring helps set prices.

This means competition is stiff and trying to outguess market prices is difficult for anyone, even professional money managers (see question 2 for more on this). This is good news for investors though. Rather than basing an investment strategy on trying to find securities that are priced “incorrectly,” investors can instead rely on the information in market prices to help build their portfolios (see question 5 for more on this).

* Year-end WM/Reuter’s London Close FX rates used to convert original US dollars data to British pound sterling.

Source: World Federation of Exchanges members, affiliates, correspondents, and non-members. Trade data from the global electronic order book. Daily averages were computed using year-to-date totals as of December 31, 2016, divided by 250 as an approximate number of annual trading days.

What are my chances of picking an investment fund that survives and outperforms?

Flip a coin and your odds of getting heads or tails are 50/50. Historically, the odds of selecting an investment fund that was still around 15 years later are about the same. Regarding outperformance, the odds are worse. The market’s pricing power works against fund managers who try to outperform through stock picking or market timing. One needn’t look further than real-world results to see this. Based on research, only 17% of US equity mutual funds and 18% of US fixed income mutual funds have survived and outperformed their benchmarks over the past 15 years.

Source: Mutual Fund Landscape 2017, Dimensional Fund Advisors. See Appendix for important details on the study.

Past performance is no guarantee of future results.

If I choose a fund because of strong past performance, does that mean it will do well in the future?

Some investors select mutual funds based on past returns. However, research shows that most funds in the top quartile (25%) of previous five-year returns did not maintain a top-quartile ranking in the following year. In other words, past performance offers little insight into a fund’s future returns.

Source: Mutual Fund Landscape 2017, Dimensional Fund Advisors. See Appendix for important details on the study.

Past performance is no guarantee of future results.

Do I have to outsmart the market to be a successful investor?

Financial markets have rewarded long-term investors. People expect a positive return on the capital they invest, and historically, the equity and bond markets have provided growth of wealth that has more than offset inflation. Instead of fighting markets, let them work for you.

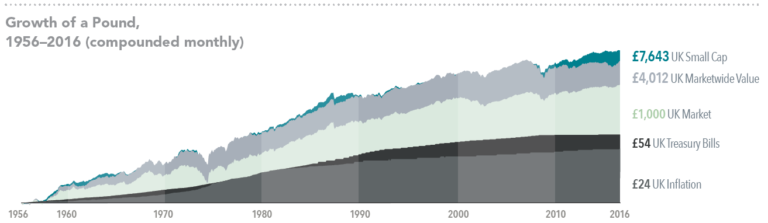

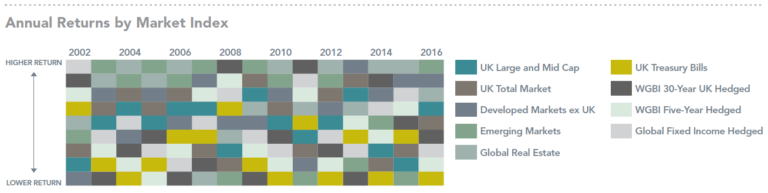

In British pound sterling. UK Small Cap is the Dimensional UK Small Cap Index. UK Marketwide Value is the Dimensional UK Marketwide Value Index. UK Market is the Dimensional UK Market Index. UK Treasury Bills are UK One-Month Treasury Bills. UK Inflation is the UK Retail Price Index. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio. See appendix for index descriptions.

Past performance is no guarantee of future results. The graph is for illustrative purposes only, figures presented are hypothetical and not indicative of any investment.

Is there a better way to build a portfolio?

Academic research has identified these equity and fixed income dimensions, which point to differences in expected returns among securities. Instead of attempting to outguess market prices, investors can instead pursue higher expected returns by structuring their portfolio around these dimensions.

Relative price is measured by the price-to-book ratio; value stocks are those with lower price-to-book ratios. Profitability is measured as operating income before depreciation and amortisation minus interest expense scaled by book.

Is international investing for me?

Diversification helps reduce risks that have no expected return, but diversifying only within your home market may not be enough. Instead, global diversification can broaden your investment opportunity set. By holding a globally diversified portfolio, investors are well positioned to seek returns wherever they occur.

International investing involves special risks such as currency fluctuation and political instability. Investing in emerging markets may accentuate these risks. Diversification neither assures a profit nor guarantees against loss in a declining market.

Will making frequent changes to my portfolio help me achieve investment success?

It’s tough, if not impossible, to know which market segments will outperform from period to period.

Accordingly, it’s better to avoid market timing calls and other unnecessary changes that can be costly. Allowing emotions or opinions about short-term market conditions to impact long-term investment decisions can lead to disappointing results.

Past performance is no guarantee of future results.

Should I make changes to my portfolio based on what I’m hearing in the news?

Daily market news and commentary can challenge your investment discipline. Some messages stir anxiety about the future, while others tempt you to chase the latest investment fad. If headlines are unsettling, consider the source and try to maintain a long-term perspective.

So, what should I be doing?

Work closely with a financial adviser who can offer expertise and guidance to help you focus on actions that add value. Focusing on what you can control can lead to a better investment experience.

Create an investment plan to fit your needs and risk tolerance.

Structure a portfolio along the dimensions of expected returns.

Diversify globally.

Manage expenses, turnover, and taxes.

Stay disciplined through market dips and swings.

Please feel free to contact us if you would like a no cost, no obligation appraisal of your current portfolio(s).

APPENDIX

Question 2: The sample includes US mutual funds at the beginning of the 15-year period ending December 31, 2016. Each fund is evaluated relative to the Morningstar benchmark assigned to the fund’s category at the start of the evaluation period. Surviving funds are those with return observations for every month of the sample period. Winner funds are those that survived and whose cumulative net return over the period exceeded that of their respective Morningstar category benchmark.

Question 3: At the end of each year, US mutual funds are sorted within their category based on their five-year total return. US mutual funds in the top quartile (25%) of returns are evaluated again in the following year based on one-year performance in order to determine the percentage of funds that maintained a top-quartile ranking. The analysis is repeated each year from 2007– 2016. The chart shows average persistence of top-quartile funds during the 10-year period.

Question 4: DIMENSIONAL UK SMALL CAP INDEX: January 1994–present: Compiled from Bloomberg securities data. Market capitalisation-weighted index of small company securities in the eligible markets excluding those with the lowest profitability and highest relative price within the small cap universe. Profitability is measured as operating income before depreciation and amortisation minus interest expense scaled by book. Exclusions: REITs and investment companies. The index has been retroactively calculated by Dimensional Fund Advisors and did not exist prior to April 2008. The calculation methodology for the Dimensional UK Small Cap Index was amended in January 2014 to include direct profitability as a factor in selecting securities for inclusion in the index. July 1981–December 1993: Includes securities in the bottom 10% of market capitalisation, excluding the bottom 1%. Rebalanced semiannually. Prior to July 1981: Elroy Dimson and Paul Marsh, Hoare Govett Smaller Companies Index 2009, ABN-AMRO/Royal Bank of Scotland, January 2009.

DIMENSIONAL UK MARKETWIDE VALUE INDEX: January 1994–present: Compiled from Bloomberg securities data. The index consists of companies whose relative price is in the bottom 33% of their country’s companies after the exclusion of utilities and companies with either negative or missing relative price data. The index emphasises companies with smaller capitalisation, lower relative price and higher profitability. The index also excludes those companies with the lowest profitability and highest relative price within their country’s value universe. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. Exclusions: REITs and investment companies. The index has been retroactively calculated by Dimensional Fund Advisors and did not exist prior to April 2008. The calculation methodology for the Dimensional UK Value Index was amended in January 2014 to include direct profitability as a factor in selecting securities for inclusion in the index. Prior to January 1994: Source: Dimson, Elroy, Stevan Nagel and Garrett Quigley. 2003. “Capturing the value premium in the UK”, Financial Analysts Journal 2003, 59(6): 35–45. Created Returns, converted from GBP to USD using the WM/Reuters at 4 pm EST (closing spot), from PFPC exchange rate.

DIMENSIONAL UK MARKET INDEX: Compiled by Dimensional from Bloomberg securities data. Market capitalisation-weighted index of all securities in the United Kingdom. Exclusions: REITs and investment companies. The index has been retroactively calculated by Dimensional and did not exist prior to April 2008.

UK ONE-MONTH TREASURY BILLS: Provided by the Financial Times Limited. Prior to 1975: UK Three-Month Treasury Bills provided by the London Share Price Database.

UK RETAIL PRICE INDEX: Provided by the Office for National Statistics; Crown copyright material is reproduced with the permission of the Controller of HMSO.

Manage Cookie Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behaviour or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.